Small Caps Defy the Yield Shock

The Russell 2000 has surged 12 percent in the first quarter of 2026 while the S&P 500 has fallen 4 percent, as the widest valuation gap in a generation and a projected 43 percent earnings growth rate draw capital into domestic small-cap equities.

The First Quarter Divergence

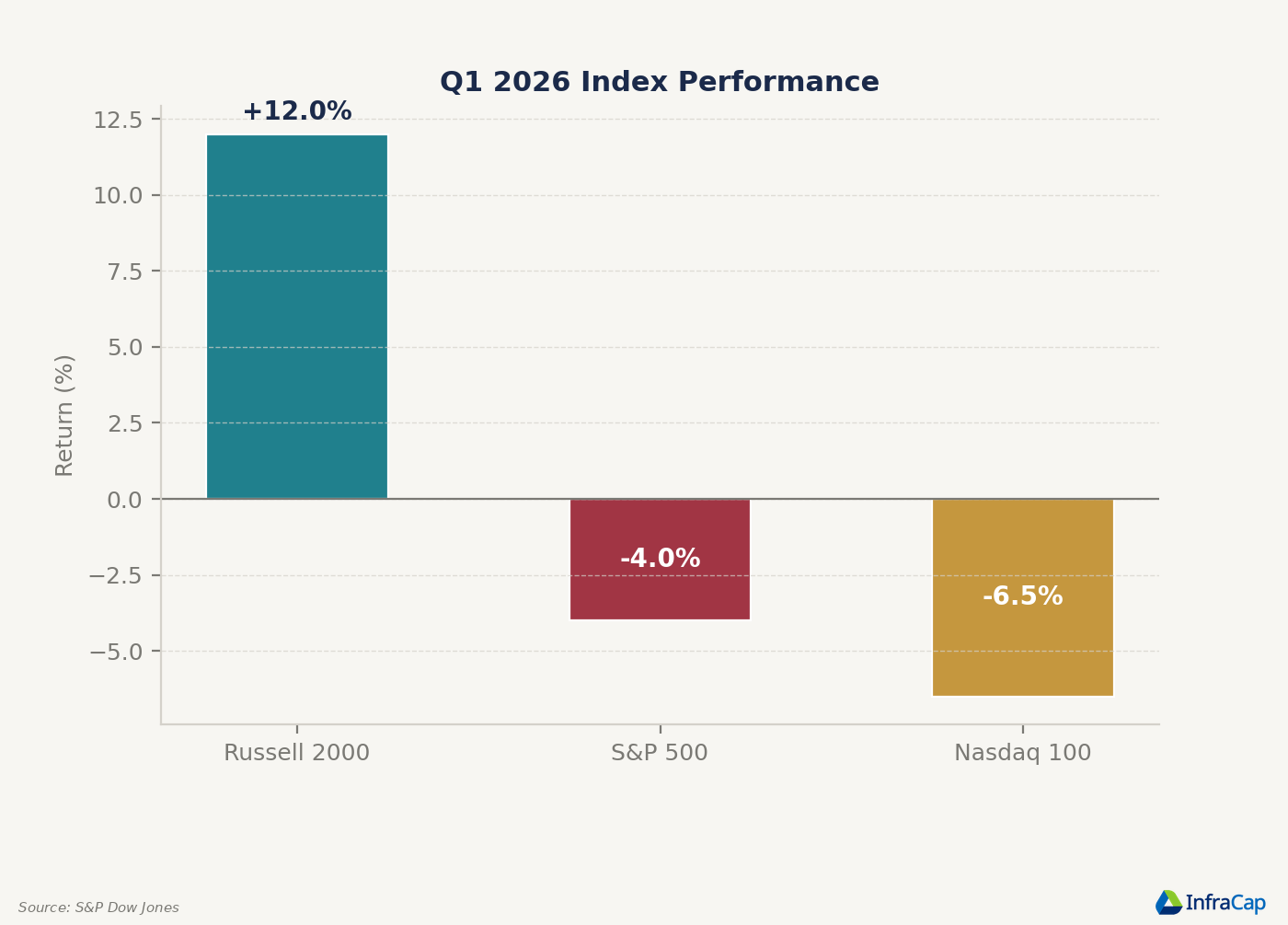

The Russell 2000 gained approximately 12 percent in the first quarter of 2026, while the S&P 500 declined roughly 4 percent. The performance gap of 16 percentage points represents the widest quarterly divergence in favor of small caps since the post-pandemic reopening trade of late 2020.¹

The rally was not linear. Small caps surged in January, posting a 15-session winning streak against large caps. A 10 percent technical correction followed in February as Treasury yields spiked. The March rebound was swift, with the Russell 2000 climbing back to 2,505 by March 24 as institutional investors rotated capital out of mega-cap technology names and into the domestic economy.²

The Nasdaq-100, weighed down by what analysts have termed "AI capex fatigue," struggled as investors questioned the near-term return on massive infrastructure spending. The tech-heavy index underperformed both the Russell 2000 and the S&P 500 for the quarter, marking a regime change in equity leadership.

The Russell 2000 gained approximately 12% in Q1 2026, while the S&P 500 fell 4% and the Nasdaq-100 lagged further. Source: S&P Dow Jones

Valuation and Earnings Drive the Case

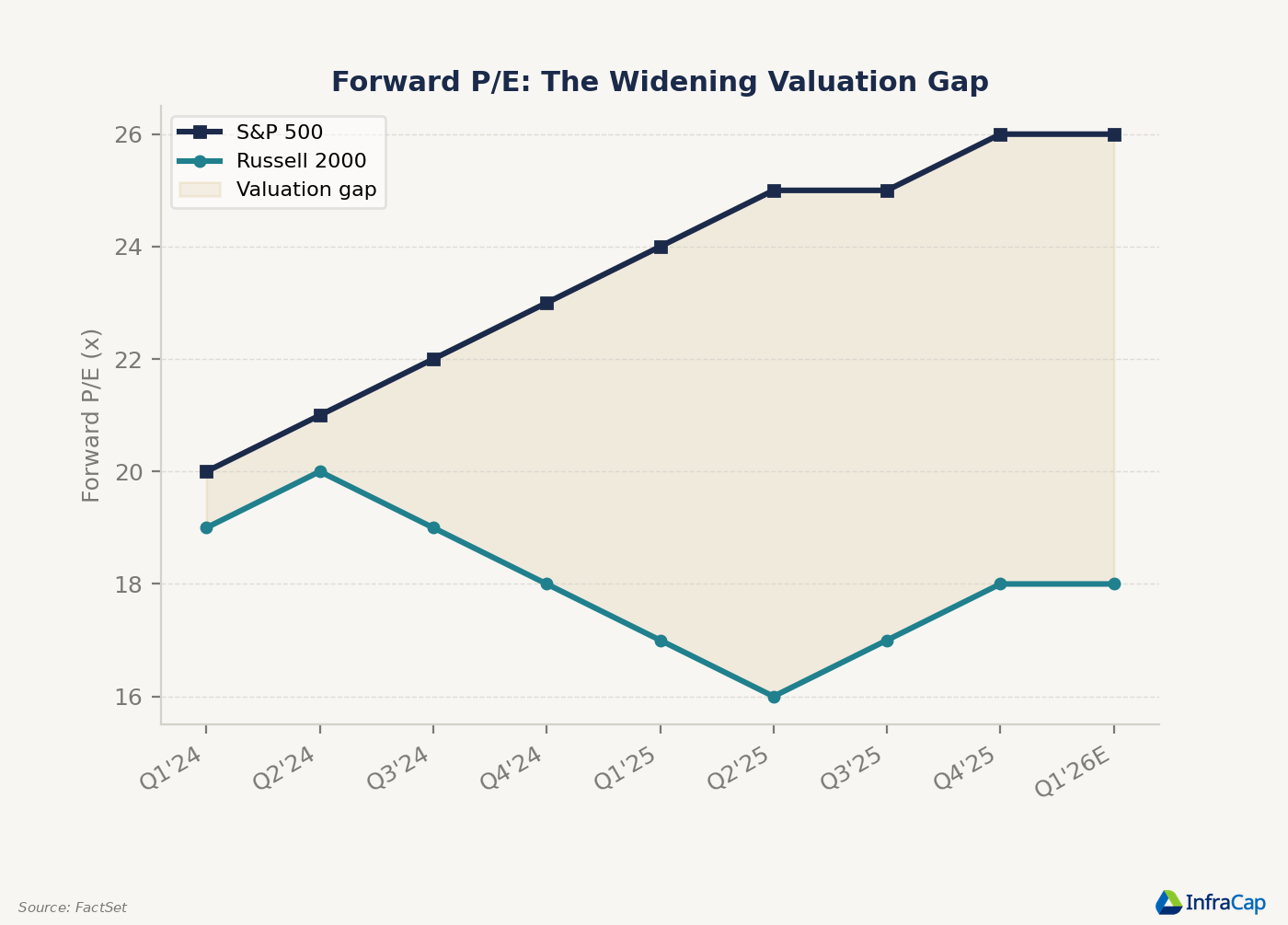

The Russell 2000 entered 2026 trading at approximately 18 times forward earnings, compared to 26 times for the S&P 500. The 30 percent-plus discount represented the widest valuation gap in over 25 years. Before the pandemic, small caps typically commanded a premium to large caps. That premium has been absent for nearly five years.³

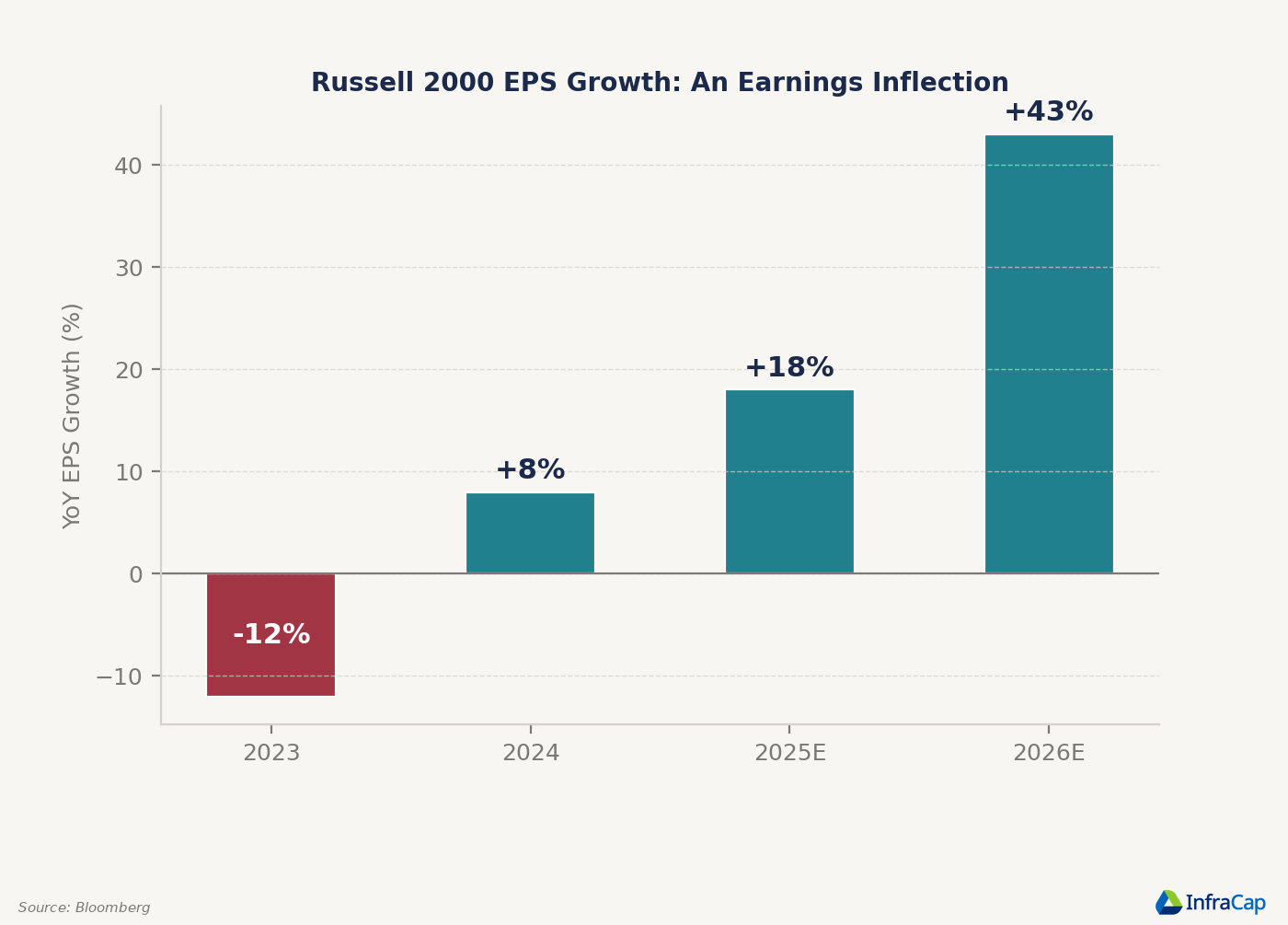

Earnings growth projections have reinforced the rotation. Bloomberg consensus estimates as of January 2026 project the Russell 2000 to deliver 43 percent year-over-year earnings growth over the coming twelve months. The Russell 2500 is expected to grow by 18 percent, while the S&P 500 is projected at 11 percent. The earnings inflection, after negative growth in 2023 and 2024, is drawing fundamental investors back to the asset class.⁴

The passage of the One Big Beautiful Bill Act in mid-2025 provided additional tailwinds. The legislation restored immediate research and development expensing and 100 percent bonus depreciation while shifting the interest deduction limit from 30 percent of EBIT to 30 percent of EBITDA. For capital-intensive small-cap manufacturers, these changes translated directly into improved cash flow.

The forward P/E discount of small caps vs. large caps reached its widest level in over 25 years heading into 2026. Source: FactSet

Floating-Rate Risk Meets Fiscal Tailwind

The yield environment remains the primary risk for small-cap investors. With approximately 40 percent of Russell 2000 debt carrying floating rates, the 10-year Treasury yield's climb to 4.44 percent has raised refinancing costs. The $368 billion maturity wall in 2026 requires many index constituents to refinance at rates near 6.5 percent, roughly triple the pandemic-era levels.⁵

The counterweight is the breadth of the earnings recovery. Small-cap industrials and biotechs are projected to see 18 to 35 percent earnings increases in the 2026 fiscal year. Regional banks, a significant component of the Russell 2000, benefit from a steeper yield curve even as loan quality concerns linger. The shift toward "growth at a reasonable price" has brought institutional capital back to a segment of the market that was largely ignored during the mega-cap technology run.⁶

The first quarter has demonstrated that small caps can generate meaningful returns even in a rising-rate environment, provided earnings growth is strong enough to offset the cost of capital. The valuation discount, domestic fiscal support, and earnings inflection represent a combination of tailwinds that has not existed simultaneously since the early 2000s.

Russell 2000 earnings growth is projected at 43% for the coming 12 months, after negative growth in 2023 and 2024. Source: Bloomberg

Footnotes

1. S&P Dow Jones Indices, Russell 2000 and S&P 500 factsheets, March 24, 2026.

2. Chronicle Journal, The Great Rotation: Russell 2000 Outshines Mega-Caps, March 24, 2026.

3. FactSet Earnings Insight, Forward P/E Estimates, March 2026.

4. Columbia Threadneedle, Why Own US Small Caps in 2026, March 17, 2026.

5. Goldman Sachs Research, Small-Cap Equity Outlook, March 2026.

6. American Century, Global Small-Caps Trends in 2026, January 2026.

About Us

Jay D. Hatfield is CEO of Infrastructure Capital Advisors and is the lead portfolio manager of the Infrastructure Capital Bond Income ETF (NYSE: BNDS), InfraCap Small Cap Income ETF (NYSE: SCAP), InfraCap Equity Income Fund ETF (NYSE: ICAP), InfraCap MLP ETF (NYSE: AMZA), Virtus InfraCap U.S. Preferred Stock ETF (NYSE: PFFA), InfraCap REIT Preferred ETF (NYSE: PFFR) and private funds. Each month Infrastructure Capital hosts a monthly economic webinar; you can sign up to attend by visiting our website www.infracapfunds.com (important disclosures can also be found on the website). For a prospectus please reach out to us or visit the links above for each respective fund.

DISCLOSURE

This information is not an offer to sell, or solicitation of an offer to buy any investment product, security, or services offered by Jay Hatfield, or Infrastructure Capital Advisors, LLC, (”ICA”) or its affiliates. ICA, will only conduct such solicitation of an offer to buy any investment product or service offered by ICA, if at all, by (1) purported definitive documentation (which will include disclosures relating to investment objective, policies, risk factors, fees, tax implications and relevant qualifications), (2) to qualified participants, if applicable, and (3) only in those jurisdictions where permitted by law. Jay Hatfield or ICA may have a beneficial long or short position in securities discussed either through stock ownership, options, or other derivatives; nonetheless, under no circumstances does any article or interview represent a recommendation to buy or sell these securities. This discussion is intended to provide insight into stocks and the market for entertainment and information purposes only and is not a solicitation of any kind. ICA buys and sells securities on behalf of its fund investors and may do so, before and after any particular article herein is published, with respect to the securities discussed in any article posted. ICA’s appraisal of a company (price target) is only one factor that affects its decision whether to buy or sell shares in that company. Other factors might include, but are not limited to, the presence of mandatory limits on individual positions, decisions regarding portfolio exposures, and general market conditions and liquidity needs. As such, there may not always be consistency between the views expressed here and ICA’s trading or holdings on behalf of its fund investors. There may be conflicts between the content posted or discussed and the interests of ICA. Please reach out to the ICA for more information. Investors should make their own decisions regarding any investments mentioned, and the information here is not a substitute for obtaining professional advice from a licensed financial professional. Investing involves risk including the loss of principal invested. Past performance is not a guarantee of future results. The information herein is provided by Infrastructure Capital Advisors, LLC (the “Adviser”), a Registered Investment Adviser and the investment adviser to the InfraCap ETFs. The information is based upon sources believed to be reliable but is not guaranteed as to accuracy.

The information contained herein represents our subjective belief and opinions and should not be construed as investment, tax, legal, or financial advice. Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. Please read the prospectus carefully before investing. For more information about the Fund, Fund strategies or Infrastructure Capital, please reach out to Craig Starr at 212-763-8336 (Craig.Starr@icmllc.com). The Funds are distributed either by Quasar Distributors, LLC or by VP Distributors, LLC, an affiliate of Virtus ETF Advisers, LLC. ICAP, SCAP, and BNDS ETFs are distributed by Quasar Distributors LLC. PFFA, PFFR, and AMZA ETFs are distributed by VP Distributors, LLC an affiliated of Virtus ETF Advisers, LLC.