The historical benefits of passive indexing are well established in the equity world. According to S&P Dow Jones Indices' latest SPIVA data, 76.26% of all U.S. large-cap active funds underperformed the S&P 500® Index over the five years ending December 31, 2024.

Similar trends hold across most traditional equity categories and geographies, where liquidity is deep, analyst coverage is broad, and information is quickly priced in. These are all factors that make it increasingly difficult for active equity managers to consistently outperform. But that is not the case across all asset classes. In segments such as preferred securities, where liquidity is thinner, issuance terms vary widely, and institutional coverage is far more limited, we believe active management continues to offer advantages.

The Virtus InfraCap U.S. Preferred Stock ETF (PFFA) is one example of how a hands-on, research-driven approach may deliver value in this underappreciated corner of the market.

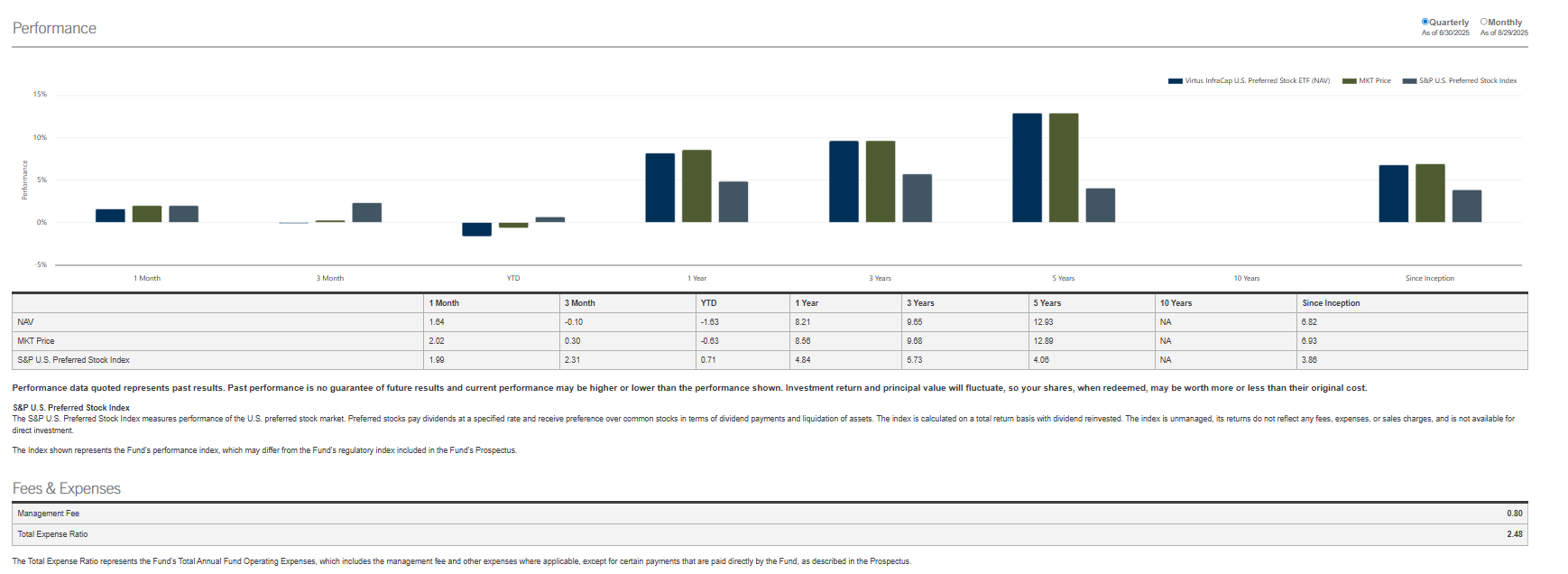

PFFA: Outperformance Versus Index Benchmarks

For the five-year period ending 6/30/25, PFFA delivered an average annual NAV return of 12.93%. That stands in sharp contrast to the 4.06% average annual return from the S&P U.S. Preferred Stock Index over the same period.

Investors who chose a passive benchmark alternative would have faced half a decade of effectively flat performance. And clipping coupons alone would not have closed the gap.

Notably, neither of these preferred stock indices incurs management fees or fund-level operating expenses. PFFA did, and still finished well ahead.

What Made (and Makes) PFFA Different

Indexing preferreds may appear efficient, but the methodology behind most benchmarks is not well suited to this hybrid asset class. Take the S&P U.S. Preferred Stock Index, for example. Its inclusion screens focus on size and volume, both liquidity constraints.

Once a preferred security passes those hurdles, it gets in regardless of rate type (fixed, floating, or variable), structure (cumulative or not), or features (callable or convertible). From there, securities are simply weighted by market cap, with a 10% cap per issuer. That works well in equities. In preferreds, it opens the door to two structural problems.

The first problem is sector concentration. Banks issue preferreds frequently, to manage regulatory capital adequacy ratios, so they dominate the index. Today, financials make up nearly 72% of the S&P U.S. Preferred Stock Index. There is nothing fundamentally wrong with bank preferreds, but a methodology based only on size may end up creating portfolios that are far from diversified.

Second is the issue of negative yield-to-call. Preferreds are often callable at par, but may trade above par in the market. For example, a security callable at $25 in three years might be trading at $27. If called, the investor would lose $2 in principal, which could more than offset any dividends received.

Indices cannot dynamically avoid these situations. But active strategies like PFFA can. That helps set this Fund apart.

The portfolio construction process considers sector exposure, screens out negative yield-to-call positions, and actively diversifies across sectors such as real estate, mortgage REITs, industrials, and utilities. Financials are still present, but not as dominant.

To help raise the 30-day SEC yield to 9.73% (as of June 30, 2025), PFFA also employs modest leverage, typically around 20–30%. This can boost beta and income generation in environments where the team believes the risk-reward profile is attractive.

Preferreds are often overlooked, and many investors who see flat performance from passive benchmarks may write off the space entirely. But strategies like PFFA show that active management still has a role, especially when the structure of the asset class calls for it.

Please consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The prospectus contains this and other information about the Fund. Contact us at 1-888-383-0553 or visit www.virtus.com for a copy of the Fund's prospectus. Read the prospectus carefully before you invest or send money.

Inception Date: Standard performance is displayed from Virtus InfraCap US Preferred Stock ETF’s inception date of October 15, 2018.

Exchange-Traded Funds (ETF): The value of an ETF may be more volatile than the underlying portfolio of securities it is designed to track. The costs to the portfolio of owning shares of an ETF may exceed the cost of investing directly in the underlying securities. Preferred Stocks: Preferred stocks may decline in price, fail to pay dividends, or be illiquid. Leverage: When the Fund leverages its portfolio, the Fund may be less liquid and/or may liquidate positions at an unfavorable time, and the value of the Fund’s shares will be more volatile and sensitive to market movements. Non-Diversified: The portfolio is not diversified and may be more susceptible to factors negatively impacting its holdings to the extent the portfolio invests more of its assets in the securities of fewer issuers than would a diversified portfolio. Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss. Market Volatility: The value of the securities in the portfolio may go up or down in response to the prospects of individual companies and/or general economic conditions. Local, regional, or global events such as war or military conflict, terrorism, pandemic, or recession could impact the portfolio, including hampering the ability of the portfolio’s manager(s) to invest its assets as intended. Prospectus: For additional information on risks, please see the fund’s prospectus. PFFA is distributed by VP Distributors, LLC, member FINRA and subsidiary of Virtus Investment Partners, Inc.

DISCLOSURE

This information is not an offer to sell, or solicitation of an offer to buy any investment product, security, or services offered by Jay Hatfield, or Infrastructure Capital Advisors, LLC, (“ICA”) or its affiliates. ICA, will only conduct such solicitation of an offer to buy any investment product or service offered by ICA, if at all, by (1) purported definitive documentation (which will include disclosures relating to investment objective, policies, risk factors, fees, tax implications and relevant qualifications), (2) to qualified participants, if applicable, and (3) only in those jurisdictions where permitted by law. Jay Hatfield or ICA may have a beneficial long or short position in securities discussed either through stock ownership, options, or other derivatives; nonetheless, under no circumstances does any article or interview represent a recommendation to buy or sell these securities. This discussion is intended to provide insight into stocks and the market for entertainment and information purposes only and is not a solicitation of any kind. ICA buys and sells securities on behalf of its fund investors and may do so, before and after any particular article herein is published, with respect to the securities discussed in any article posted. ICA's appraisal of a company (price target) is only one factor that affects its decision whether to buy or sell shares in that company. Other factors might include, but are not limited to, the presence of mandatory limits on individual positions, decisions regarding portfolio exposures, and general market conditions and liquidity needs. As such, there may not always be consistency between the views expressed here and ICA's trading or holdings on behalf of its fund investors. There may be conflicts between the content posted or discussed and the interests of ICA. Please reach out to the ICA for more information. Investors should make their own decisions regarding any investments mentioned, and their prospects based on such investors’ own review of publicly available information and should not rely on the information contained herein. ICA nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. We have not sought, nor have we received, permission from any third-party to include their information in this article. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or other comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.

The information contained herein represents our subjective belief and opinions and should not be construed as investment, tax, legal, or financial advice. Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. Please read the prospectus carefully before investing. For more information about the Fund, Fund strategies or Infrastructure Capital, please reach out to Craig Starr at 212-763-8336 (Craig.Starr@icmllc.com). The Funds are distributed either by Quasar Distributors, LLC or by VP Distributors, LLC, an affiliate of Virtus ETF Advisers, LLC. ICAP, SCAP, and BNDS ETFs are distributed by Quasar Distributors LLC. PFFA, PFFR, and AMZA ETFs are distributed by VP Distributors, LLC an affiliated of Virtus ETF Advisers, LLC.