Everyone knows that master limited partnerships (MLPs) aren’t your typical energy investments. Their pass-through tax structure, large quarterly distributions, and focus on midstream assets like pipelines set them apart from upstream oil explorers or downstream refiners.

But beyond those structural differences, what really matters is the bottom line: how do MLPs compare on risk and return over time? Have they actually been the better part of the energy sector to invest in for the long haul? We think the data makes a strong case. Here’s why.

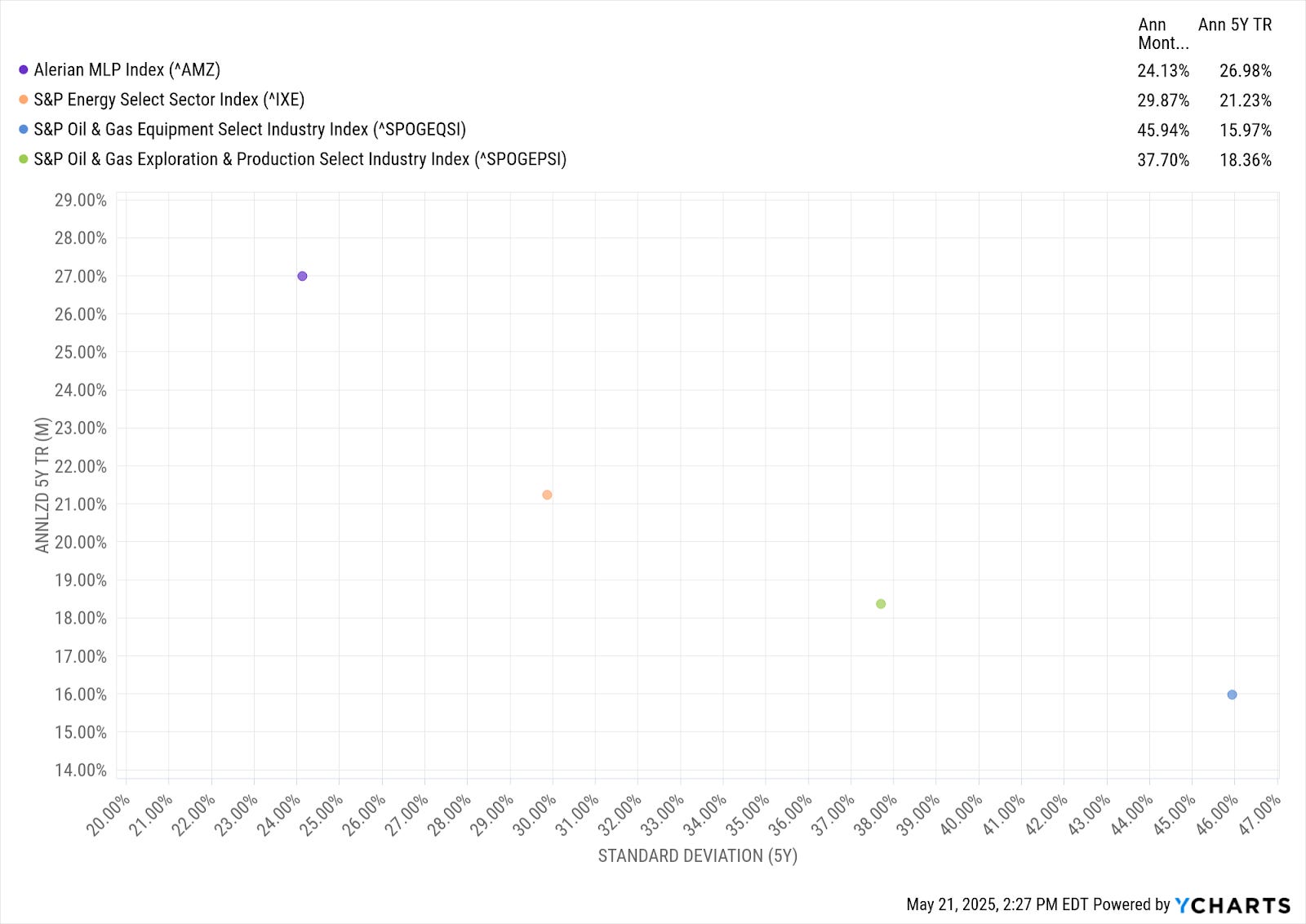

MLPs Have Outperformed with Less Risk

The Alerian MLP Index (AMZ) tracks midstream master limited partnerships, which generate most of their revenue by transporting and storing oil, gas, and refined products.

The S&P Energy Select Sector Index (IXE) is a market-cap weighted benchmark of large U.S. energy companies, dominated by integrated majors like ExxonMobil (XOM) and Chevron (CVX).

The S&P Oil & Gas Equipment Select Industry Index (SPOGEQSI) captures oilfield services and drilling contractors, names like Schlumberger (SLB), Baker Hughes (BKR).

Meanwhile, the S&P Oil & Gas Exploration & Production Index (SPOGEPSI) is made up of upstream energy firms like ConocoPhillips (COP) focused on finding and extracting oil and gas.

Over the five-year window ending in May 2025, a period marked by extreme dislocations, from the COVID-19 oil collapse to Russia’s invasion of Ukraine and ongoing conflict in the Middle East, MLPs outperformed across the board.

AMZ delivered a 26.98% annualized total return with just 24.13% volatility. That’s a stronger result than IXE’s 21.23% return and 29.87% volatility, and far more favorable than the higher-risk, lower-return profiles of SPOGEQSI and SPOGEPSI.

Why MLPs Are Structurally More Solid

Ceteris paribus, meaning all else equal (there are always exceptions), we believe MLPs are positioned to continue offering a mix of attractive returns and relatively lower volatility thanks to some structural advantages built into their business models.

The energy sector is no stranger to turbulence. For companies involved in exploration and production, revenues are highly sensitive to commodity prices. If oil prices drop, their top line gets hit almost immediately, as the product they sell is now worth less.

Downstream refiners and chemical firms, while sometimes cushioned by refining margins, also face risk from narrowing spreads, fluctuating input costs, and demand swings. Volumes and pricing can both be volatile, and that variability flows straight into the financial statements.

Now contrast that with the typical MLP. These businesses operate energy infrastructure: pipelines, storage tanks, and terminals. Rather than profiting off commodity prices directly, they earn fees based on volumes transported or stored, often through long-term, fee-based contracts.

That means if oil prices drop but producers still need to move product, pipeline operators keep collecting. Cash flow is steadier, more visible, and more contractually locked in than in many other parts of the energy sector. That reliable income stream is what allows MLPs to pay above-average distributions and keep volatility lower.

Of course, MLPs are not low-risk by any means. They face regulatory scrutiny, especially around environmental impact, and pipelines can become political flashpoints. Changes in tax policy or shifts in energy transition sentiment can affect valuations. And like any other asset, poor management or overleveraged can erode investor returns.

But on the whole, for investors seeking exposure to the energy sector without the boom-bust rollercoaster of producers or oil services, MLPs offer a strong alternative. You still get commodity-linked upside, but through a steadier toll booth model, one that historically has paid you to stay the course.

About Us

Jay D. Hatfield is CEO of Infrastructure Capital Advisors and is the lead portfolio manager of the Infrastructure Capital Bond Income ETF (NYSE: BNDS), InfraCap Small Cap Income ETF (NYSE: SCAP), InfraCap Equity Income Fund ETF (NYSE: ICAP), InfraCap MLP ETF (NYSE: AMZA), Virtus InfraCap U.S. Preferred Stock ETF (NYSE: PFFA), InfraCap REIT Preferred ETF (NYSE: PFFR) and private funds. Each month Infrastructure Capital hosts a monthly economic webinar; you can sign up to attend by visiting our website www.infracapfunds.com (important disclosures can also be found on the website). For a prospectus please reach out to us or visit the links above for each respective fund.

DISCLOSURE

This information is not an offer to sell, or solicitation of an offer to buy any investment product, security, or services offered by Jay Hatfield, or Infrastructure Capital Advisors, LLC, (“ICA”) or its affiliates. ICA, will only conduct such solicitation of an offer to buy any investment product or service offered by ICA, if at all, by (1) purported definitive documentation (which will include disclosures relating to investment objective, policies, risk factors, fees, tax implications and relevant qualifications), (2) to qualified participants, if applicable, and (3) only in those jurisdictions where permitted by law. Jay Hatfield or ICA may have a beneficial long or short position in securities discussed either through stock ownership, options, or other derivatives; nonetheless, under no circumstances does any article or interview represent a recommendation to buy or sell these securities. This discussion is intended to provide insight into stocks and the market for entertainment and information purposes only and is not a solicitation of any kind. ICA buys and sells securities on behalf of its fund investors and may do so, before and after any particular article herein is published, with respect to the securities discussed in any article posted. ICA's appraisal of a company (price target) is only one factor that affects its decision whether to buy or sell shares in that company. Other factors might include, but are not limited to, the presence of mandatory limits on individual positions, decisions regarding portfolio exposures, and general market conditions and liquidity needs. As such, there may not always be consistency between the views expressed here and ICA's trading or holdings on behalf of its fund investors. There may be conflicts between the content posted or discussed and the interests of ICA. Please reach out to the ICA for more information. Investors should make their own decisions regarding any investments mentioned, and their prospects based on such investors’ own review of publicly available information and should not rely on the information contained herein. ICA nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. We have not sought, nor have we received, permission from any third-party to include their information in this article. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or other comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.

The information contained herein represents our subjective belief and opinions and should not be construed as investment, tax, legal, or financial advice. Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. Please read the prospectus carefully before investing. For more information about the Fund, Fund strategies or Infrastructure Capital, please reach out to Craig Starr at 212-763-8336 (Craig.Starr@icmllc.com). The Funds are distributed either by Quasar Distributors, LLC or by VP Distributors, LLC, an affiliate of Virtus ETF Advisers, LLC. ICAP, SCAP, and BNDS ETFs are distributed by Quasar Distributors LLC. PFFA, PFFR, and AMZA ETFs are distributed by VP Distributors, LLC an affiliated of Virtus ETF Advisers, LLC.