How Infrastructure and Reshoring Trends Could Benefit Underserved Small-Cap Players

The drone of construction equipment has become a recognizable sound in once-quiet industrial towns. In De Soto, Kansas, Panasonic’s new $4 billion electric vehicle (EV) battery plant—the largest private investment in Kansas history—is projected to create up to 4,000 jobs and generate roughly $2.5 billion in annual economic activity¹. The same types of stories are playing out across the country. This resurgence is driven by a dual engine: a wave of manufacturing reshoring and historic infrastructure investment.

Re-shoring: The Supply Chain Comes Home

It used to be a political slogan — “Made in America” — but it’s now an economic reality. The COVID-19 crisis revealed vulnerability in the global supply chain, and geopolitical rivalry pushed companies toward localization. US manufacturing investments announced through 2025 have already surpassed $1.2 trillion in semiconductors, electronics and clean energy².

This trend has been magnified by policy incentives such as the CHIPS Act and clean-energy tax credits. Companies including Micron and Panasonic are building mega-facilities — as well as seeding networks of smaller contractors, from electricians to trucking companies³. The reshoring discussion is no longer about nostalgic longing, but rather national resilience and regional development.

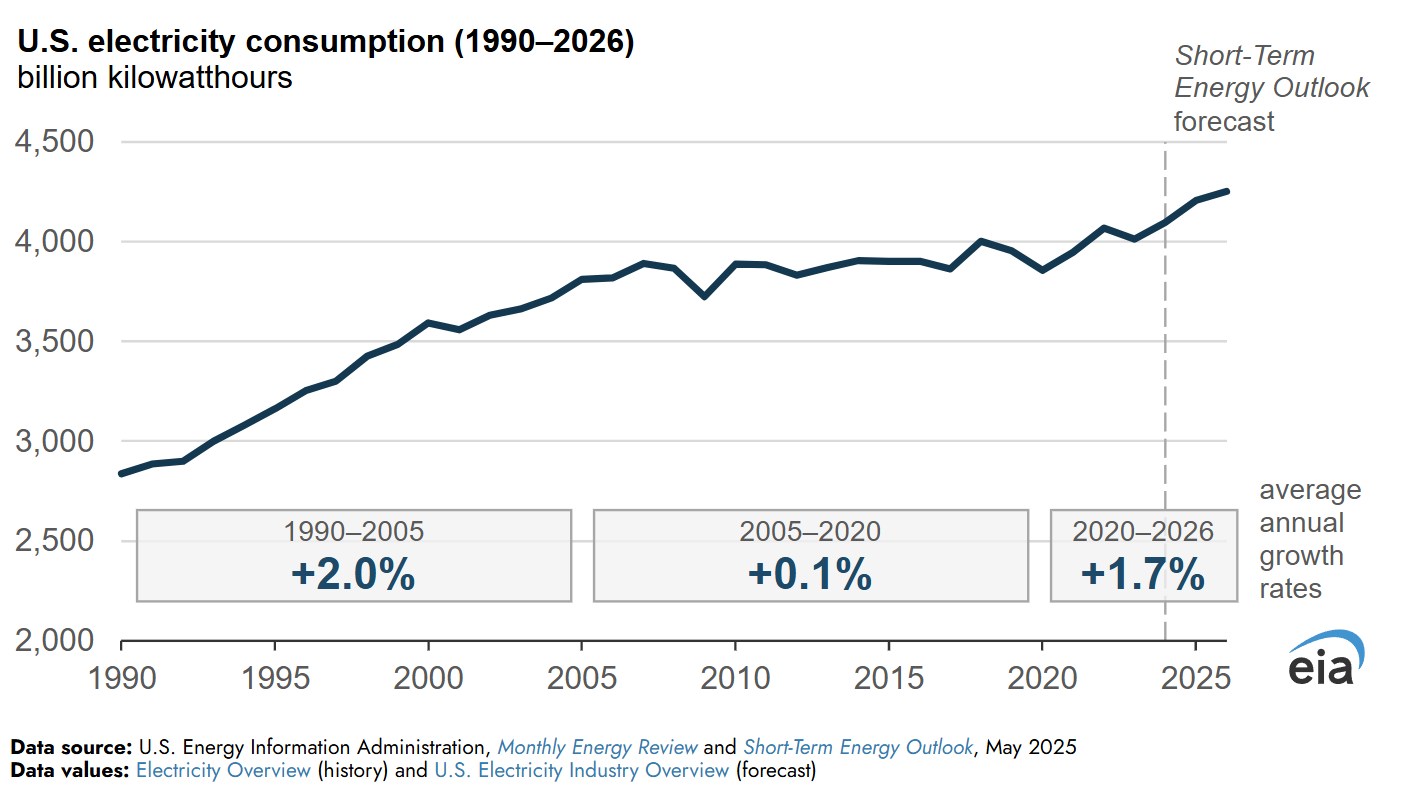

Infrastructure Investment: Building the Backbone

Reshoring aligns with Washington’s multiyear infrastructure overhaul. The Infrastructure Investment and Jobs Act (IIJA) and related legislation are channeling hundreds of billions into roads, bridges, power grids, and broadband. For small and mid-sized enterprises, these public projects represent substantial tailwinds.

Take the U.S. power grid: after years of stagnation, electricity demand is projected to grow nearly 5% over the next five years⁴. Expanding EV adoption and factory electrification require upgraded grids, transformers, and transmission systems. Small-cap construction, engineering, and materials firms stand to benefit from these multi-year contracts and local project pipelines.

The Small-Cap Opportunity

The macro story is obvious: America is beginning to invest in itself again. It’s small-cap stocks, which tend to be much more domestically focused than their larger brethren, that stand to gain disproportionately. Small-cap outperformance has historically followed periods of infrastructure-fueled growth. Today, these equities continue to trade at discounts to large caps⁵ providing investors with an opportunity for asymmetric upside as deglobalization and reindustrialization themes persist.

That said, investors will need to be selective. There are risks, specifically high borrowing costs, shortages of both skilled and unskilled labor and project delays. The winners may well be those with strong balance sheets and niche expertise in infrastructure supply chains or industrial services.

Conclusion: America’s Small Giants

From Kansas to upstate New York, a manufacturing and infrastructure revival is underway. For the first time in years, the “little guys” of American industry have structural winds at their backs. While execution challenges remain, the convergence of reshoring and infrastructure investment offers fertile ground for discerning investors looking beyond Wall Street’s usual suspects.

Footnotes

“Officials Celebrate Grand Opening of Panasonic EV Battery Plant in De Soto,” KSHB 41 Kansas City, July 14, 2025, https://www.kshb.com/news/local-news/updates-panasonic-ev-battery-plant-grand-opening-celebration-underway-in-de-soto.

Mike Rode, “How Does U.S. Policy Influence the Reshoring Surge?” American Century Investments, July 31, 2025.

Madeline Ruid, “Manufacturing Revival Creates Tailwinds for U.S. Infrastructure Spending,” Global X ETFs, October 15, 2025.

U.S. Federal Energy Regulatory Commission (FERC), Electric Power Demand Outlook, 2025–2030.

Russell Investments, “Are Small Caps Next in Line to Shine?” July 9, 2025, https://russellinvestments.com/content/ri/us/en/insights/russell-research/2025/07/small-caps-next-in-line.html.

About Us

Jay D. Hatfield is CEO of Infrastructure Capital Advisors and is the lead portfolio manager of the Infrastructure Capital Bond Income ETF (NYSE: BNDS), InfraCap Small Cap Income ETF (NYSE: SCAP), InfraCap Equity Income Fund ETF (NYSE: ICAP), InfraCap MLP ETF (NYSE: AMZA), Virtus InfraCap U.S. Preferred Stock ETF (NYSE: PFFA), InfraCap REIT Preferred ETF (NYSE: PFFR) and private funds. Each month Infrastructure Capital hosts a monthly economic webinar; you can sign up to attend by visiting our website www.infracapfunds.com (important disclosures can also be found on the website). For a prospectus please reach out to us or visit the links above for each respective fund.

DISCLOSURE

This information is not an offer to sell, or solicitation of an offer to buy any investment product, security, or services offered by Jay Hatfield, or Infrastructure Capital Advisors, LLC, (“ICA”) or its affiliates. ICA, will only conduct such solicitation of an offer to buy any investment product or service offered by ICA, if at all, by (1) purported definitive documentation (which will include disclosures relating to investment objective, policies, risk factors, fees, tax implications and relevant qualifications), (2) to qualified participants, if applicable, and (3) only in those jurisdictions where permitted by law. Jay Hatfield or ICA may have a beneficial long or short position in securities discussed either through stock ownership, options, or other derivatives; nonetheless, under no circumstances does any article or interview represent a recommendation to buy or sell these securities. This discussion is intended to provide insight into stocks and the market for entertainment and information purposes only and is not a solicitation of any kind. ICA buys and sells securities on behalf of its fund investors and may do so, before and after any particular article herein is published, with respect to the securities discussed in any article posted. ICA’s appraisal of a company (price target) is only one factor that affects its decision whether to buy or sell shares in that company. Other factors might include, but are not limited to, the presence of mandatory limits on individual positions, decisions regarding portfolio exposures, and general market conditions and liquidity needs. As such, there may not always be consistency between the views expressed here and ICA’s trading or holdings on behalf of its fund investors. There may be conflicts between the content posted or discussed and the interests of ICA. Please reach out to the ICA for more information. Investors should make their own decisions regarding any investments mentioned, and their prospects based on such investors’ own review of publicly available information and should not rely on the information contained herein. ICA nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. We have not sought, nor have we received, permission from any third-party to include their information in this article. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or other comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.

The information contained herein represents our subjective belief and opinions and should not be construed as investment, tax, legal, or financial advice. Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. Please read the prospectus carefully before investing. For more information about the Fund, Fund strategies or Infrastructure Capital, please reach out to Craig Starr at 212-763-8336 (Craig.Starr@icmllc.com). The Funds are distributed either by Quasar Distributors, LLC or by VP Distributors, LLC, an affiliate of Virtus ETF Advisers, LLC. ICAP, SCAP, and BNDS ETFs are distributed by Quasar Distributors LLC. PFFA, PFFR, and AMZA ETFs are distributed by VP Distributors, LLC an affiliated of Virtus ETF Advisers, LLC.