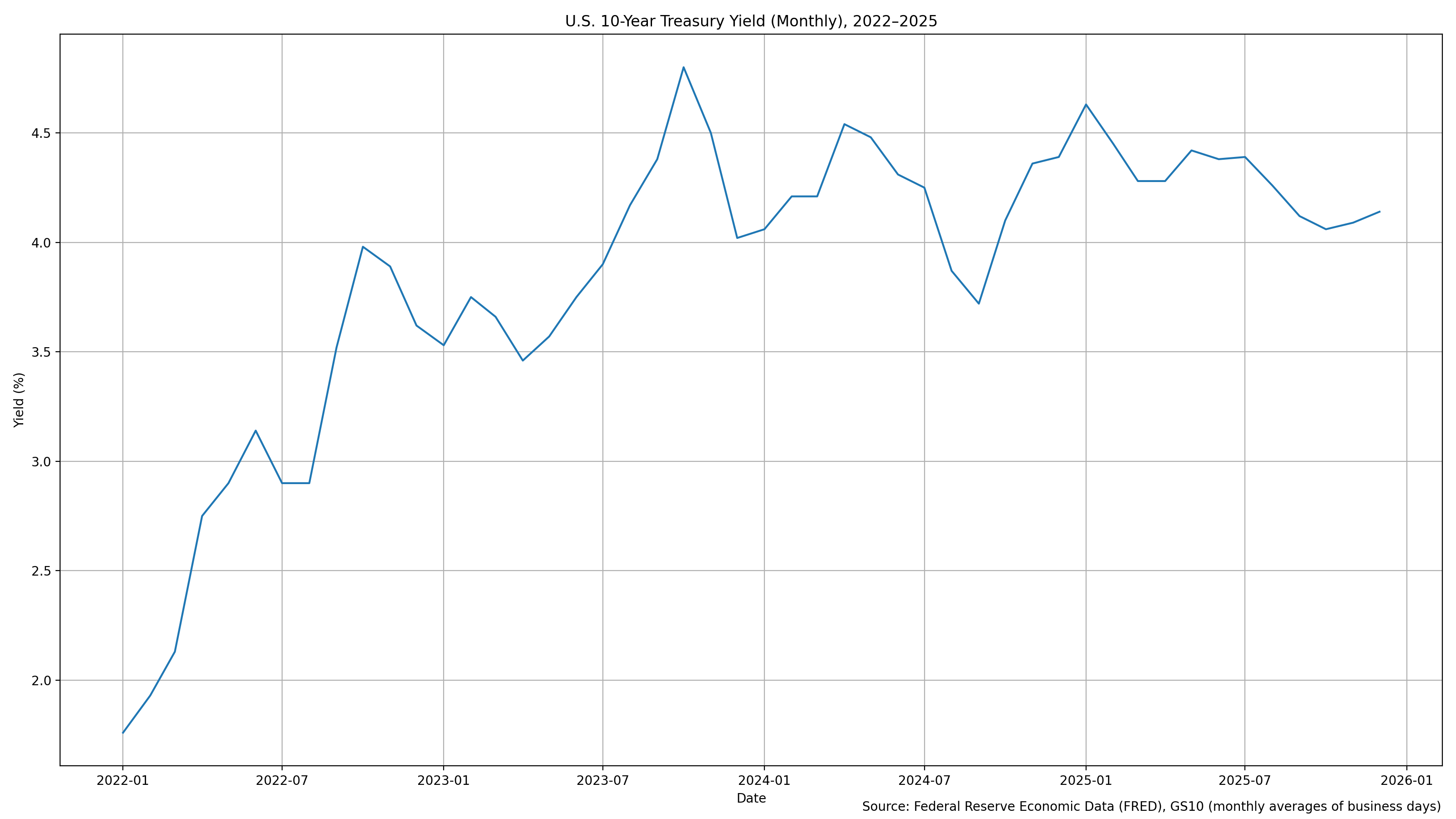

Equities tied to artificial intelligence and technology continue to dominate market attention, but the bond market may be setting up for a steadier, less visible opportunity in 2026. After the U.S. 10-year Treasury yield surged to multi-decade highs in late 2023, yields reversed meaningfully by year-end, signaling that the tightening cycle may have peaked.¹ If rates have indeed crested, fixed-income investors may benefit from a combination of coupon income and modest price appreciation. With policymakers increasingly focused on sustaining growth rather than suppressing inflation at all costs, bonds appear positioned to reclaim their traditional role as a stabilizing portfolio anchor rather than a source of volatility.

Managing Duration in a Shifting Rate Cycle

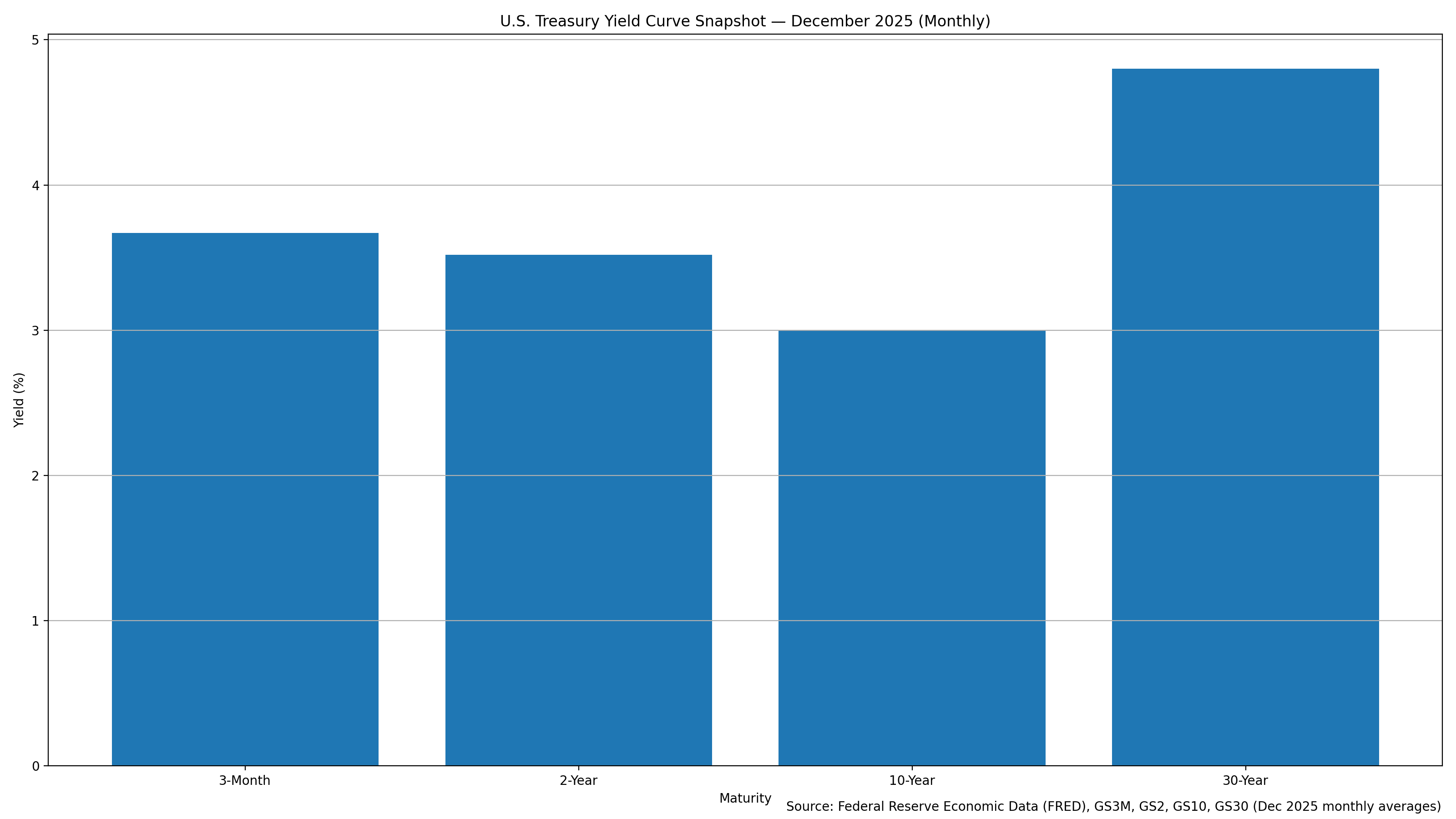

Interest-rate policy remains the most important driver of bond returns heading into 2026. Market consensus anticipates a gradual easing path as inflation pressures moderate, bringing short-term rates lower over time.² That environment generally favors duration, but not aggressively. Several research houses describe the outlook as range-bound rather than directional, suggesting that large bets at either end of the yield curve may prove counterproductive.³

A neutral, intermediate-term duration stance offers balance. It allows investors to participate if rates drift lower while limiting downside if inflation proves sticky or growth reaccelerates. Bond ladders remain a practical tool in this environment, providing predictable cash flows while continuously reinvesting maturities at prevailing yields.⁴ This structure reduces timing risk and supports disciplined income generation without requiring precise rate forecasts.

Credit Discipline and Selective Yield

Credit selection may matter more than duration in 2026. Credit spreads remain compressed by historical standards, leaving little margin for error if economic conditions soften. Research from major brokerages continues to emphasize an up-in-quality bias, favoring investment-grade corporate bonds where balance sheets remain resilient.⁵ Lower-quality segments, including high-yield corporates and floating-rate loans, could face pressure if earnings weaken or refinancing costs remain elevated.⁶

For investors seeking incremental income, selective allocations beyond core government and corporate bonds can still play a role. Higher-yielding sectors such as emerging-market debt, structured credit, or bank loans may enhance portfolio income, but position sizing and diversification are essential.⁷ Municipal bonds also remain compelling in taxable accounts, where tax-adjusted income compares favorably with many corporate alternatives.⁸ Across all sectors, the emphasis should remain on issuer quality and structural protections rather than headline yield.

Putting the Framework Together

A sound bond strategy for 2026 starts with high-quality, intermediate-term holdings as the foundation. From there, modest, well-researched yield enhancements can improve income without materially increasing portfolio risk. Cash or short-duration bonds provide flexibility should volatility return. Above all, patience and discipline matter. The objective is not to chase price gains, but to earn carry, manage risk, and allow bonds to quietly do what they are designed to do.⁹

Footnotes

RBC Wealth Management, “Have Bonds Rallied Too Far, Too Fast?” December 18, 2023.

BlackRock iShares, “Fed Outlook 2026: Rate Forecasts and Fixed Income Strategies,” December 4, 2025.

LPL Research, “Navigating Neutral Fed Policy: Key for Fixed Income Markets in 2026,” November 21, 2025.

BlackRock iShares, “Fed Outlook 2026: Rate Forecasts and Fixed Income Strategies,” December 4, 2025.

Schwab Center for Financial Research, “Schwab Center for Financial Research Reveals Its 2026 Market Outlook,” December 11, 2025.

LPL Research, “Navigating Neutral Fed Policy: Key for Fixed Income Markets in 2026,” November 21, 2025.

BlackRock iShares, “Fed Outlook 2026: Rate Forecasts and Fixed Income Strategies,” December 4, 2025.

Schwab Center for Financial Research, “Schwab Center for Financial Research Reveals Its 2026 Market Outlook,” December 11, 2025.

PineBridge Investments, “2026 Fixed Income Outlook: Stay Calm and Keep Your Carry On,” December 2, 2025.

About Us

Jay D. Hatfield is CEO of Infrastructure Capital Advisors and is the lead portfolio manager of the Infrastructure Capital Bond Income ETF (NYSE: BNDS), InfraCap Small Cap Income ETF (NYSE: SCAP), InfraCap Equity Income Fund ETF (NYSE: ICAP), InfraCap MLP ETF (NYSE: AMZA), Virtus InfraCap U.S. Preferred Stock ETF (NYSE: PFFA), InfraCap REIT Preferred ETF (NYSE: PFFR) and private funds. Each month Infrastructure Capital hosts a monthly economic webinar; you can sign up to attend by visiting our website www.infracapfunds.com (important disclosures can also be found on the website). For a prospectus please reach out to us or visit the links above for each respective fund.

DISCLOSURE

This information is not an offer to sell, or solicitation of an offer to buy any investment product, security, or services offered by Jay Hatfield, or Infrastructure Capital Advisors, LLC, (“ICA”) or its affiliates. ICA, will only conduct such solicitation of an offer to buy any investment product or service offered by ICA, if at all, by (1) purported definitive documentation (which will include disclosures relating to investment objective, policies, risk factors, fees, tax implications and relevant qualifications), (2) to qualified participants, if applicable, and (3) only in those jurisdictions where permitted by law. Jay Hatfield or ICA may have a beneficial long or short position in securities discussed either through stock ownership, options, or other derivatives; nonetheless, under no circumstances does any article or interview represent a recommendation to buy or sell these securities. This discussion is intended to provide insight into stocks and the market for entertainment and information purposes only and is not a solicitation of any kind. ICA buys and sells securities on behalf of its fund investors and may do so, before and after any particular article herein is published, with respect to the securities discussed in any article posted. ICA’s appraisal of a company (price target) is only one factor that affects its decision whether to buy or sell shares in that company. Other factors might include, but are not limited to, the presence of mandatory limits on individual positions, decisions regarding portfolio exposures, and general market conditions and liquidity needs. As such, there may not always be consistency between the views expressed here and ICA’s trading or holdings on behalf of its fund investors. There may be conflicts between the content posted or discussed and the interests of ICA. Please reach out to the ICA for more information. Investors should make their own decisions regarding any investments mentioned, and their prospects based on such investors’ own review of publicly available information and should not rely on the information contained herein. ICA nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. We have not sought, nor have we received, permission from any third-party to include their information in this article. Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or other comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.

The information contained herein represents our subjective belief and opinions and should not be construed as investment, tax, legal, or financial advice. Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. Please read the prospectus carefully before investing. For more information about the Fund, Fund strategies or Infrastructure Capital, please reach out to Craig Starr at 212-763-8336 (Craig.Starr@icmllc.com). The Funds are distributed either by Quasar Distributors, LLC or by VP Distributors, LLC, an affiliate of Virtus ETF Advisers, LLC. ICAP, SCAP, and BNDS ETFs are distributed by Quasar Distributors LLC. PFFA, PFFR, and AMZA ETFs are distributed by VP Distributors, LLC an affiliated of Virtus ETF Advisers, LLC.